In our last post, we talked about the Employer Mandate. What is it? Does it apply to me? And what about those terrifying penalties? Now that we’ve established what is required and for whom, it’s time to move on to the next step towards compliance: reporting! Though Employer Mandate reporting may seem like a behemoth of a task, taking a minute to break everything down can prove well worth the effort. Here we’ll discuss different reporting requirements for different employer demographics, reporting methods, and solutions to help ease the burden of ACA tracking and reporting.

Reporting Requirements

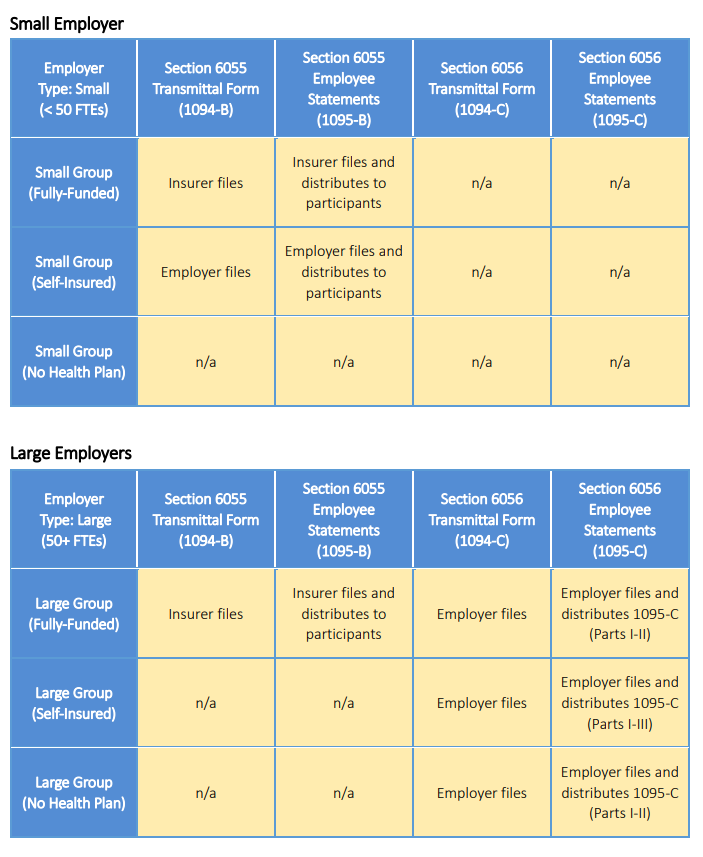

Under the ACA, employers with 50+ full-time equivalent employees and small self-funded groups must complete Employer Mandate reporting. This requirement went into effect in 2016, so we now have several years of experience under our belts.

Generally, just like with W-2’s, employers must provide their employees copies of these forms by January 31st. However, this year, the IRS extended this deadline to March 4. The deadline to file with the IRS is February 28th, unless submitting electronically (deadline is April 1st). The IRS requires employers to file electronically unless they are submitting fewer than 250 1095-C forms for the year.

Large Employers (Fully-Insured or No Coverage)

Section 6056 of the Tax Code requires:

- One Transmittal Form (IRS Form 1094-C)

- Employee Statements (IRS Form 1095-C, Sections I & II only)

Large Employers (Self-Funded)

Sections 6055 & 6056 of the Tax Code require:

- One Transmittal Form (IRS Form 1094-C)

- Employee Statements (IRS Form 1095-C, Sections I-III)

Small Employers (Self-Funded)

- One Transmittal Form (IRS Form 1094-B)

- Employee Statements (IRS Form 1095-B)

Top Tip: It may help you to think of the 1094-C as similar to the W-3 (a transmittal form) and the 1095-C as similar to the W-2 (a separate return for each employee).

Small Employers (Fully-Insured or No Coverage)

No reporting required.

Sections 6055 & 6056 Reporting: Who Does What?

Three Methods of Reporting

General Method

The General Method requires the greatest amount of information collection for Employer Mandate reporting. All large employers with 50+ full-time equivalent employees must use this method unless they qualify for reporting relief (see the two alternative reporting methods below).

When using the General Method, the employer must file a 1094-C for the company and 1095-Cs for each employee. The employee must also receive a copy of the 1095-C.

Employers required to use this method must collect the following data for reporting purposes:

- Employer name, address, and Tax ID.

- Name and phone number of the employer’s contact person responsible for health insurance (may be either an employee or an agent of the employer).

- The calendar year for the information reported.

- Certification as to whether the employer provided a plan that meets the minimum value requirement to full-time employees and their dependents by calendar month.

- The months that a plan that meets the minimum value requirement was available to each full-time employee.

- Each full-time employee’s monthly cost for employee-only coverage under the employer’s least expensive minimum value plan (bronze level or higher).

- The number of full-time employees employed each month in the calendar year.

- Name, address, and Tax ID of each full-time employee employed during the calendar year.

- Months each employee was covered on the group health plan during the year.

Qualifying Offer Method

In an attempt to ease the Employer Mandate reporting burden for employers who offer a plan that meets the minimum value requirement at a very low rate, the government offers such employers the option to report a bit less information. An employer may take advantage of this option if it provides a “qualifying offer” of insurance to any of its full-time employees. A qualifying offer is an offer of a bronze level or higher plan where the cost to the employee of employee-only coverage is less than $96.08/month in 2018 or $99.75/month in 2019. Also, the employer must offer the plan to all members of the employee’s family to be eligible to use this reporting method.

So how is Employer Mandate reporting different when using this method?

For employees who receive qualifying offers for all 12 months of the year, employers will need to report only the names, addresses, and tax ID numbers of those employees and the fact that they received a full-year qualifying offer. Additionally, the employer does not have to report how much the employee contributed to the plan each month.

For employees who receive qualifying offers for fewer than 12 months of the year, the employer may use a code for each month a qualifying offer was made.

98% Offer Method

To offer some reporting relief to reward employers offering to at least 98% of the company’s full-time employees a bronze level or higher plan at an “affordable” rate, the IRS provides the 98% Offer Method.

So how is this method of Employer Mandate reporting different from the General Method?

The employer does not have to identify which employees regularly work full-time hours. Rather, the employer is simply required to include in the report those who may be full-time.

A Simpler Solution

Feeling a little overwhelmed? The best part is, you don’t have to! Southland Data Processing’s ACA solution is a complete healthcare compliance and reporting solution. Our ACA Interactive Dashboard and skilled consulting team use your payroll data to:

- Send automated alert emails, notifying benefit administrators to take action.

- Generate advanced sub-reports with applicable suggested offer dates.

- Pre-populate forms, including the indicator codes for Form 1094/1095-C fulfillment and IRS filing.

- Review official inquiries and manage any IRS Notices or Audit Responses.

- Provide you with important analytical data and visual employee segment tracking.

What do you think?

Want to learn more about Southland Data Processing’s unique ACA solution? Let us know and we’d be happy to schedule a quick demo!

If you missed our first blog post, be sure to read up to ensure a complete understanding of your requirements heading into 2019. We hope these tips and guidelines are helpful in understanding this ACA provision. And if you’re interested in learning more about the Affordable Care Act, don’t forget to also check out our ACA Refresher in our On Demand Training Hub! Want more ways to stay up-to-date and compliant? Be sure to follow us on Facebook, Twitter, and LinkedIn to make sure you never miss a beat!

Disclaimer: The above article is intended for informational purposes only. It should not be relied upon in reaching a conclusion regarding choosing a health plan or Employer Mandate responsibility. Applicability of the principles above may differ substantially in individual situations. Please consult with your legal counsel or HR advisor prior to making any adjustments to your plans or reporting. SDP is not responsible for any inadvertent errors that may occur in the application of the Employer Mandate or Affordable Care Act.

Photo by PhotoMIX Company from Pexels