by Jannette Lajom, Partner Success Tax Supervisor

by Jannette Lajom, Partner Success Tax Supervisor

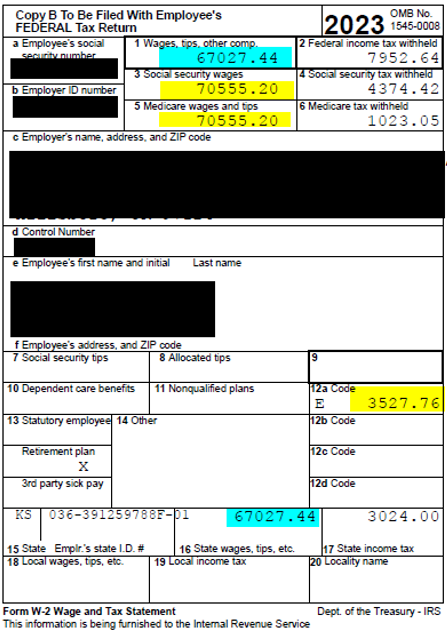

When viewing your W-2, you could easily get overwhelmed with the number of W-2 boxes. There are more than 14 of them! So, let’s get into the details:

Box 1 – Wages, tips, other compensation – This is federal, taxable income for payments in the calendar year. The amount is calculated as Year To Date (YTD) earnings minus pretax retirement and pre-tax benefit deductions plus taxable benefits (i.e., certain educational benefits).

Box 2 – Federal income tax withheld – This is federal income tax withheld from your pay based on your W-4. If you didn’t file a W-4, the default is “single and 0” regardless of your marital status.

Box 3 – Social security wages – Social security wages are calculated as Federal Taxable Gross (Box 1) plus Retirement Deductions (Box 12). The maximum social security wage amount for 2023 was $160,200.

Box 4 – Social security tax withheld – This is social security tax withheld from your pay.

Box 5 – Medicare wages and tips – This is total wages and tips subject to the Medicare component of social security taxes.

Box 6 – Medicare tax withheld – This is Medicare tax withheld from your pay for the Medicare component of social security taxes.

Box 7 – Social Security Tips – This is the total reported tips subject to social security tax.

Box 8 – Allocated Tips – This amount is not included in boxes 1,3,5 or 7.

Box 9 – Advance EIC Payments – Enter this amount on the advance earned income credit payments.

Box 10 – Dependent care benefits – This is the pre-tax deduction under the Select Benefits Program for dependent care. This deduction is already reflected in Box 1.

Box 11 – Nonqualified plans – This amount is reported in Box 1 if it is a distribution made from a nonqualified deferred compensation or nongovernmental section 457 plan.

Box 12 – Various Form W-2 codes on box 12 reflect different types of compensation or benefits. This is one of the more complex W-2 boxes, with codes ranging from A to HH. Gain more insight into W-2 box codes below.

Box 13 – If the “Retirement plan” box is checked, special limits can apply to the amount of traditional IRA contributions you can deduct.

Box 14 – Employers can use W-2 box 14 to report information such as:

- A member of the clergy’s parsonage allowance and utilities

- Any charitable contribution made through payroll deductions

- Educational assistance payments

- Health insurance premium deductions

- Nontaxable income

- State disability insurance taxes withheld

- Uniform payments

- Union dues

Since there’s no standard list of W-2 codes for Box 14, employers can list any description they choose. If the code is unclear, contact your employer and ask what the internal revenue code represents.

The W-2 Box 12 codes are:

- A – Uncollected Social Security Tax or Railroad Retirement Tax Act (RRTA) tax on tips.

- B – Uncollected Medicare tax on tips.

- C – Taxable costs of group-term life insurance over $50,000 (included in W-2 boxes 1,3 (up to Social Security wages base), and box 5); Taxable costs are information only

- D – Elective deferral under a Section 401(k) cash or arrangement plan. This includes a SIMPLE 401(k) arrangement.

- E – Code E includes elective deferrals under a Section 403(b) salary reduction agreement.

- F – Elective deferrals under a Section 408(k)(6) salary reduction SEP.

- G – Elective deferrals and employer contributions (including non-elective deferrals) to a Section 457(b) deferred compensation plan. You may be able to claim employer contributions the Saver’s Credit.

- H – Elective deferrals to a Section 501(c)(18)(D) tax-exempt organization plan.

- J – Nontaxable sick pay (information only, not included in W-2 boxes 1, 3, or 5)

- K – 20% excise tax on excess golden parachute payments.

- L – Substantiated employee business expense reimbursements (nontaxable).

- M – Uncollected Social Security tax or RRTA tax on taxable cost of group-term life insurance over $50,000 (former employees only).

- N – Uncollected Medicare tax on taxable cost of group-term life insurance over $50,000 (former employees only).

- P – Excludable moving expense reimbursements paid directly to a member of the U.S. Armed Forces (not included in Boxes 1, 3, or 5).

- Q – Nontaxable combat pay.

- R – Any employer contributions to your Archer medical savings account (MSA).

- S – Employee salary reduction contributions under a Section 408(p) SIMPLE. (Not included in Box 1).

- T – Employer Provided Adoption benefits (not included in Box 1

- V – Income from exercise of non-statutory stock option(s ) (included in Boxes 1, 3 (up to Social Security wage base), and 5). See Publication 525, Taxable and Nontaxable Income, for reporting requirements.

- W – Employer contributions (including amounts the employee elected to contribute using a Section 125 cafeteria plan) to your health savings account (HSA). (Not included in Box 1, 3, or 5.)

- Y – Deferrals under a Section 409A nonqualified deferred compensation plan.

- Z – Income under a nonqualified deferred compensation plan that fails to satisfy Section 409A. This amount is also included in Box 1 and is subject to an additional 20% tax plus interest.

- AA – Designated Roth contributions under a 401(k) plan. Roth contributions are not deductible; however, you may be able to claim the Saver’s Credit, Form 1040 Schedule 3, line 4. See Form 1040 Instructions for details.

- BB – Designated Roth contributions under a 403(b) plan. Roth contributions are not deductible; however, you may be able to claim the Saver’s Credit.

- DD – Code DD includes cost of employer-sponsored health coverage. Information only.

- EE – Designated Roth contributions under a governmental 457(b) plan. This amount doesn’t apply to contributions under a tax-exempt organization Section 457(b) plan. Roth contributions are not deductible; however, you may be able to claim the Saver’s Credit.

- FF – Permitted benefits under a qualified small employer health insurance reimbursement arrangement. Information only.

- GG – Income from qualified equity grants under Section 83(i). Information only. This amount is includible in gross income from qualified equity grants under section 83(i)(1)(A) for the calendar year. This amount is wages for box 1.

- HH – Aggregate deferrals under Section 83(i) elections as of the close of the calendar year. Information only.

CALCULATING FEDERAL AND STATE TAXABLE WAGES (BOXES 1 & 16)

Use your last pay stub for the year to calculate the taxable wages in Boxes 1 and 16 in your W-2. Begin with the Gross Pay YTD and make the following adjustments, if applicable:

Federal Taxable Wage – Adjustments to Gross Pay YTD:

Subtract YTD Before-Tax Deductions, which includes:

- Medical

• Dental

• Vision

• FSA Health

• FSA Dependent Care

• HSA

• Parking

• T Pass

• 403B

• 457 Plan

State Taxable Wage – Adjustments to Gross Pay YTD:

Subtract YTD Before-Tax Deductions, which includes:

- Medical

• Dental

• Vision

• FSA Health

• FSA Dependent Care

• HSA

• Parking

• T Pass

• 403B

• 457 Plan

The resulting amounts should equal Box 1 Federal Wages and Box 16 State Wages on your W-2. Some employees may see a difference between Box 1 Federal Wages and Box 16 State Wages due to the value of certain pre-tax transportation benefits.

CALCULATING SOCIAL SECURITY AND MEDICARE TAXABLE WAGES (BOXES 3 & 5)

The Social Security Wage Base for 2023 was $160,200. To determine Social Security and Medicare taxable wages on your W-2, again begin with the Gross Pay YTD from your final pay stub and make the following adjustments if applicable:

Social Security and Medicare Taxable Wage – Adjustments to Gross Pay YTD:

Subtract the following:

- Before-Tax Medical deductions YTD

- Before-Tax Dental deductions YTD

• Before-Tax Vision deductions YTD

• Before-Tax FSA Health deductions YTD

• Before-Tax FSA Dependent Care deductions YTD

• Before-Tax HSA deductions YTD

• Before-Tax Parking deductions YTD

• Before-Tax T Pass deductions YTD

As an experienced payroll partner, Southland Data Processing offers support to help keep payroll processing organized, compliant and accurate. Clients can expect to have access to a variety of resources, training and educational webinars to stay current with the latest news and information. For questions about the W-2 form, please contact us anytime!

Our payroll professionals assist our clients with payroll, workforce management, benefits administration, and human resources needs. To get started or learn more about these solutions, simply contact us today. We also invite you to meet with us today for a complimentary HR consultation and to learn how we can support objectives, overcome challenges, and address issues quickly and accurately.

For more information about our payroll services, please contact our payroll professionals at 909.946.2032. Or, click here and Let’s Talk!

For the latest updates, follow us on LinkedIn, Facebook, Twitter, YouTube, Instagram and TikTok for even more business tips and news.

*Southland Data Processing, Inc. (“SDP”) is not a law firm. This article is intended for informational purposes only and should not be relied upon in reaching a conclusion in a particular area of law. Applicability of the legal principles discussed may differ substantially in individual situations. Receipt of this or any other SDP materials does not create an attorney-client relationship. SDP is not responsible for any inadvertent errors that may occur in the publishing process.